Weichai Power (000338.SZ): US Hyperscaler Validation Represents a Milestone; Buy Rating Reiterated on AIDC Growth Prospects

Goldman Sachs Equity Research | 24 February 2026, 9:48 AM HKT

Permitting documents for OpenAI’s flagship Stargate data center in Texas, US, reveal the deployment of emergency generators powered by Baudouin, a wholly-owned subsidiary of Weichai Power. This marks a landmark endorsement of Baudouin by hyperscale data centers and reinforces our bullish outlook on Weichai’s substantial growth opportunities in the undersupplied AIDC power generator industry, as well as its potential for valuation rerating amid a pivotal shift in the company’s investment narrative. We thus reiterate our Buy rating on Weichai Power.

Key Developments

As cited by local US media from the Texas air permit filing for the Stargate data center in Abilene, the facility is equipped with 28 Baudouin-powered emergency generators (2.8 MW each) as standby power units, alongside 34 Caterpillar-powered gensets. Disclosures show the Baudouin units contribute approximately 78 MW of backup capacity, accounting for a significant share of the data center’s total permitted backup capacity of around 170 MW.

Strategic Implications

We have long emphasized that Weichai’s unique overseas positioning and promising US market opportunities constitute its core scarcity value among Chinese engine and genset manufacturers. This collaboration validates Weichai’s large engines with US hyperscalers, representing a major breakthrough for the company. While unstated in the permit document, media reports indicate Generac (GNRC, not covered by Goldman Sachs), Weichai’s key US local genset partner, is likely the generator supplier for this project. This aligns with Generac’s management comments regarding its pilot programs with two leading hyperscalers.

Upcoming Catalysts

March will see two key catalytic events for Weichai:

1. Weichai is set to release its full-year 2025 results on 26 March. We expect management to provide further guidance on the long-term outlook for its power generation business and potentially adjust segment reporting to carve out the power generation business (currently consolidated under the engine business segment) – a move consistent with the parent group’s recent announcement to establish energy & power as its seventh business unit.

2. Generac will host its 2026 Investor Day on 25 March, where we anticipate detailed disclosures on its data center strategy.

Investment Thesis

Weichai Power is China’s largest internal combustion engine manufacturer, holding approximately a 20% volume share in China’s multi-cylinder engine market, with core businesses spanning commercial vehicles (primarily heavy-duty trucks), construction machinery, agricultural equipment, marine engineering and power generation. Beyond its core engine business, Weichai has built a diversified portfolio over the years:

1. Complete vehicles and auto components, mainly through its 51%-owned subsidiaries Shaanxi Heavy-duty Motor (China’s third-largest heavy-duty truck maker) and Fast Gear (China’s largest gearbox manufacturer);

2. Agricultural equipment, operated via its 61.1%-owned subsidiary Weichai Lovol (China’s top agricultural equipment manufacturer);

3. Intelligent logistics (focused on industrial truck sales and supply chain solutions), through its 46.5%-owned subsidiary KION (KGX.DE) – the world’s second-largest industrial truck producer and largest supply chain solutions provider.

Weichai’s investment narrative has now shifted from heavy-duty trucks to AIDC power generation, supported by its comprehensive technology and product portfolio covering large engines for diesel gensets (AIDC backup power), gas gensets (onsite primary/standby power) and fuel cells (an emerging onsite power generation solution). AIDC power generation currently accounts for about 10% of Weichai’s projected 2025 net profit; we forecast this business to grow 3.3x by 2030, with its earnings contribution surging to roughly one-third of the company’s total and driving around 50% of Weichai’s incremental EPS growth through 2030. This transformative shift in the investment narrative, in our view, justifies a significant valuation rerating for Weichai, and we maintain a Buy rating on both its A-shares and H-shares.

Valuation Methodology & Price Targets

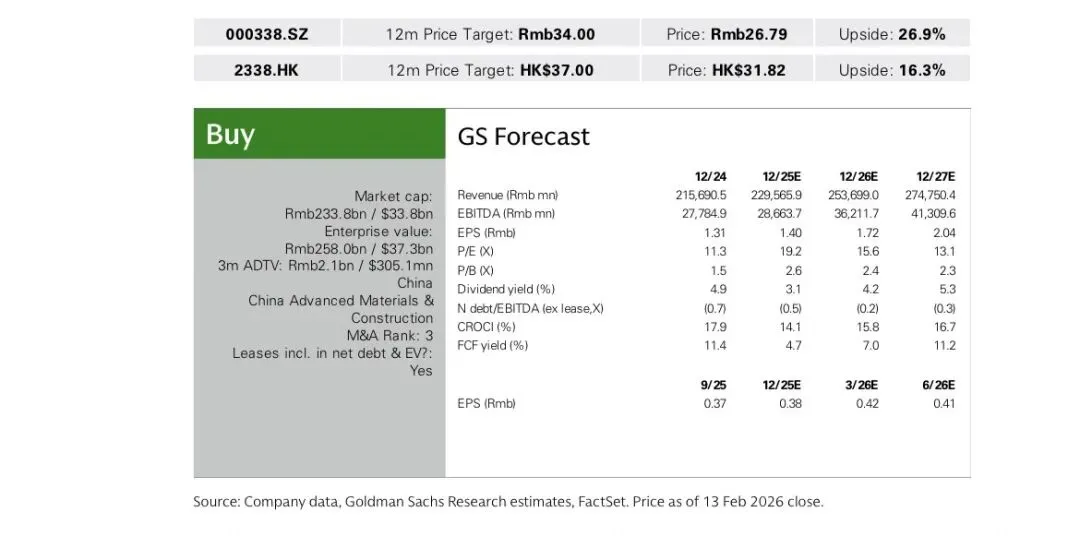

We assign a Buy rating to both Weichai’s H-shares and A-shares. For the H-shares, we value the stock at 20x its 2026E EPS, translating to a 12-month target price of HK$37.00 per share – a premium of approximately 90% over its long-term mid-cycle average of around 11x. This valuation premium reflects the shift in Weichai’s investment focus to its high-growth AIDC power generation business, with the rerating magnitude benchmarked against the valuation trends of global engine peers over the past year, while also accounting for Weichai’s stronger growth trajectory in power generation relative to its peers. For the A-shares, we apply a 1% discount to the H-share equity value, in line with the 6-month average A/H premium, leading to a 12-month target price of Rmb34.00 per share.

As of the close on 13 February 2026, Weichai’s A-shares (000338.SZ) traded at Rmb26.79 per share, implying an upside of 26.9% to our target price; its H-shares (2338.HK) were at HK$31.82 per share, with an upside of 16.3%. Weichai has a market capitalization of Rmb233.8 billion ($33.8 billion) and an enterprise value of Rmb258.0 billion ($37.3 billion), with a 3-month average daily trading volume (ADTV) of Rmb2.1 billion ($305.1 million). The company is assigned an M&A Rank of 3 (low acquisition probability, 0%-15%).

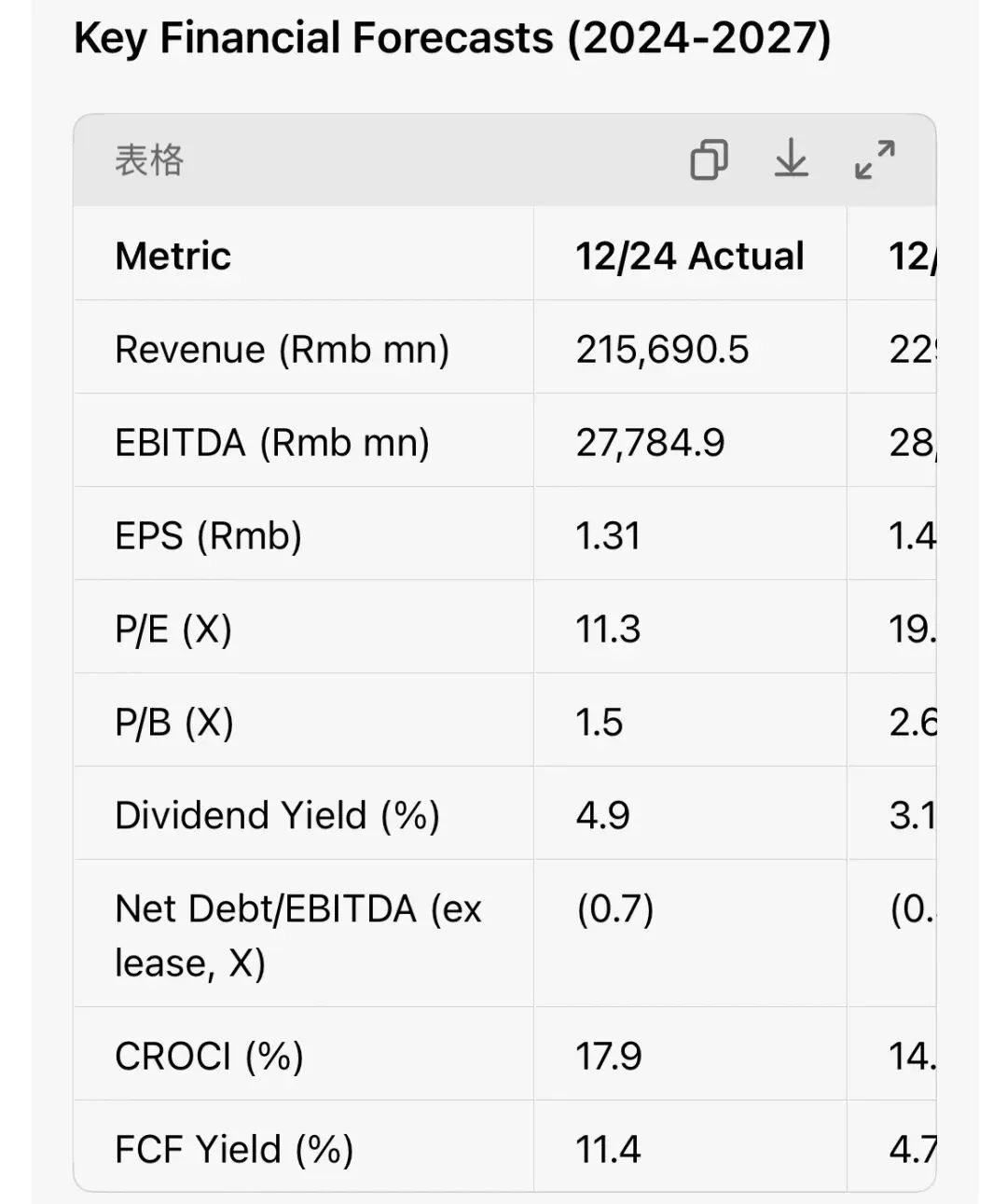

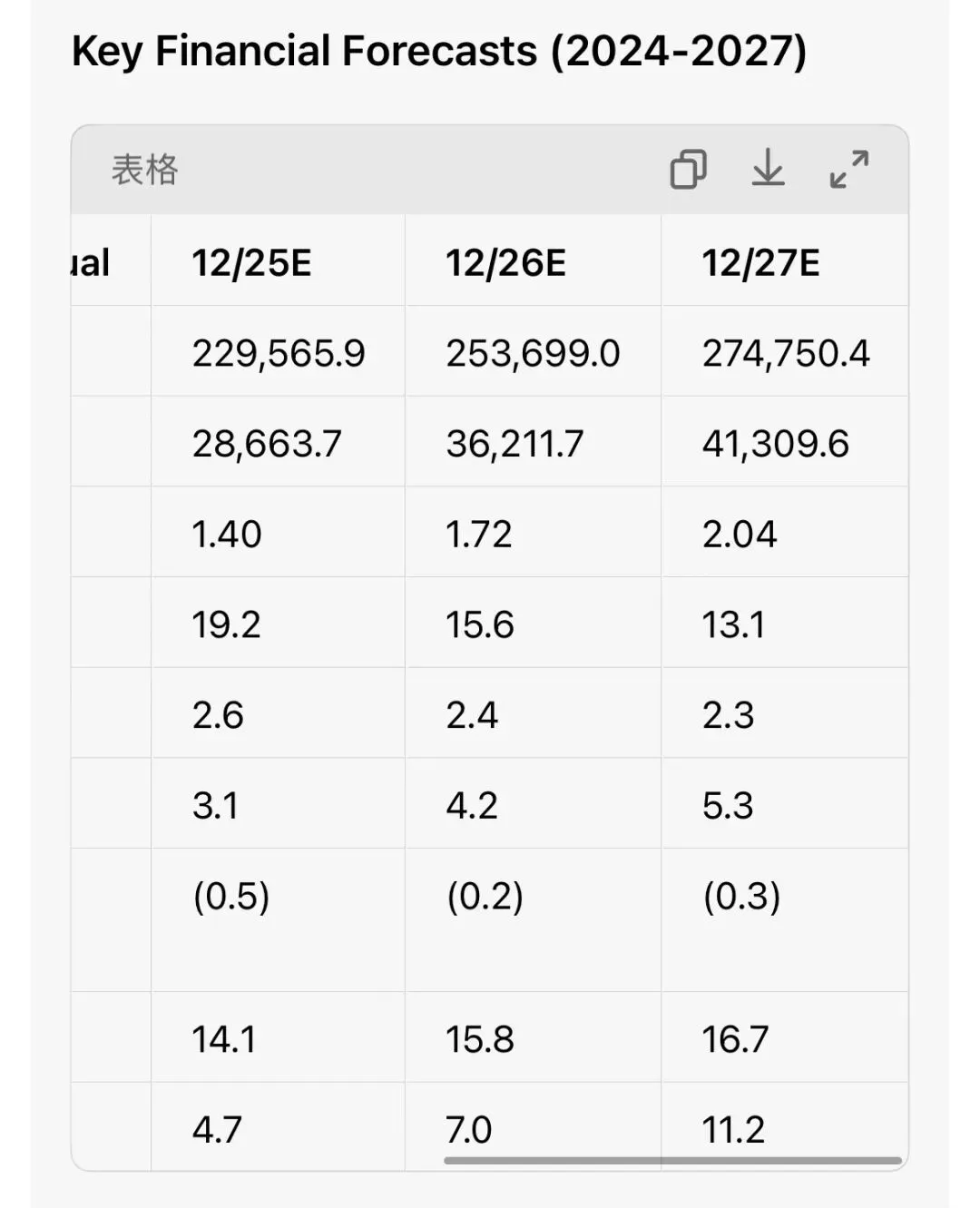

Key Financial Forecasts (2024-2027)

Key Risks

1. Slower-than-expected macroeconomic activity, particularly in road freight, infrastructure and real estate sectors;

2. Weaker global economic growth than anticipated;

3. Faster electrification penetration and lower-than-expected LNG adoption in powertrain systems;

4.Disappointing market share performance in the heavy-duty truck (HDT) engine market;

5. Slower development of the power generation business relative to our forecasts.

Regulatory & Conflict of Interest Disclosures

Goldman Sachs engages in business with the companies covered in its research reports, which may create potential conflicts of interest that impact the objectivity of this report. Investors should consider this report as only one factor in their investment decisions.

Goldman Sachs has received investment banking compensation from Generac Holdings in the past 12 months, and intends to seek or expects to receive investment banking compensation from Generac Holdings, Weichai Power A-shares and H-shares in the next three months. The firm has maintained investment banking and non-securities services client relationships with these companies over the past 12 months and acts as a market maker for their securities and related derivatives.

As of 1 January 2026, Goldman Sachs Global Investment Research has assigned investment ratings to 3,055 equity securities globally, with a rating distribution of 50% Buy, 34% Hold and 16% Sell. Among these, 65% of Buy-rated stocks, 61% of Hold-rated stocks and 46% of Sell-rated stocks have investment banking relationships with Goldman Sachs.

Goldman Sachs policy prohibits its analysts, their direct reports and household members from owning securities of covered companies. Analyst compensation is partially tied to the firm’s overall profitability, including investment banking revenues. The firm’s sales, trading and asset management teams may hold views or make investment decisions that differ from the opinions expressed in this research.

This research is for Goldman Sachs’ clients only and is based on publicly available information deemed reliable, but not guaranteed to be accurate or complete. The information, opinions and forecasts contained herein are current as of the report date and subject to change without notice. This material does not constitute an offer or solicitation to buy or sell any securities in any jurisdiction where such activity is illegal, nor a personalized investment recommendation. Investors should assess the suitability of the advice based on their own investment objectives and financial situation, and seek professional advice where necessary.