"Tencent is shifting its strategic focus to Agentic AI — autonomous systems that can execute tasks on behalf of users.""We see Tencent offering the best of both worlds: defensive characteristics through mature gaming and advertising businesses, combined with optionality through its AI investments.""Our valuation methodology rests on what we characterize as 'undemanding' metrics: Tencent trades at 17 times 2026 estimated earnings.""Tencent's AI investments will widen the gap between revenue and operating profit growth in the near term, exerting pressure on margins."

*"Tencent may not be the first mover in the AI race, but its track record shows the company repeatedly comes out ahead with better efficiency than incumbents."**"QQ OpenClaw integration marks a potential turning point for AI agent adoption in China."**"The Q4 results were solid and largely in line with our expectations."**"We expect 2026 profit growth to lag revenue growth as AI investments more than double, but this should be temporary."*

> *"We expect Tencent's Q4 2025 results will show a more positive outlook on investors' views."*> *"The key message from this earnings is not just that core businesses remain solid, but that AI has already demonstrated specific commercial value in advertising, gaming, and cloud businesses."*> *"Rather than focusing on near-term earnings forecast upgrades, we believe this earnings more importantly strengthens confidence in the company's long-term prospects."*> *"The market's focus will shift from 'is AI investment effective' to 'how much of the profits generated by AI will management choose to reinvest'."*

> *"These early-stage AI investments are likely to exert pressure on near-term margins, leading to slower profit growth compared to revenue growth in 2026."*> *"Tencent is increasing its investment in basic models, Yuanshi, and other new AI products and GPUs. These upfront investments will pressure margins in the near term, but should create new opportunities longer term."*> *"Investors are not against AI spending, but the lack of immediate monetization clarity is making them cautious."*> *"Tencent and Alibaba's latest results have exacerbated market doubts about the return on investment and profit margins for large-scale AI investments."*

> *"Tencent Holdings (0700.hk) 4Q25 review: Entering AI investment phase for the AI agentic era."*> *"AI-empowered gaming and advertising business growth prospects remain robust, driven by evergreen game record highs, advertising revenue re-acceleration (2026 YTD), and favorable app store terms potentially boosting gaming profits."*> *"We expect investors to focus on the management's guidance for AI infrastructure investment in the conference call."*

> *"Tencent Q4: Investing in an AI future."*> *"The company's core businesses are resilient, providing support for AI investments. Tencent is committed to injecting AI into social experiences."*> *"Current price at HK$550.50, with fair value estimated at HK$731.64, implying approximately 33% upside potential."*

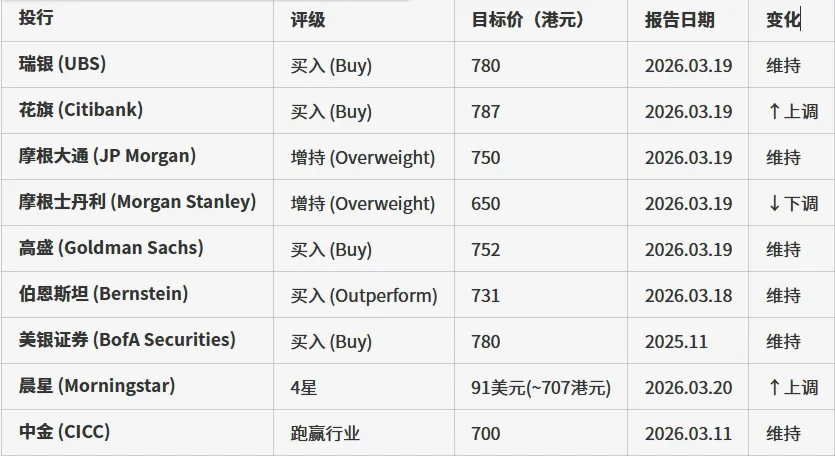

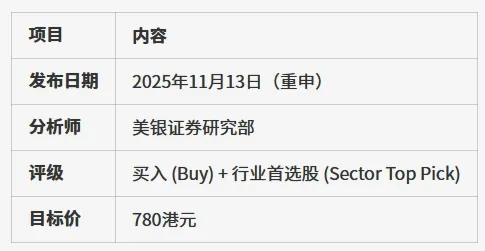

> *"Tencent remains our sector top pick, with rating at Buy and a target price of $780."*> *"AI investments combined with share buybacks will drive dual-wheel valuation recovery."*> *"Tencent's core business growth outlook remains clear."*

> *"Tencent Earnings: Accelerated Growth, Stepped-Up AI Bets."*> *"We raise wide-moat Tencent's fair value estimate by 1% to $91 per share, as higher advertising and cloud revenue more than offset increased AI investments."*> *"The stock trades at approximately 25% discount to our fair value estimate."*