Oil prices have surged from US$60/bbl at the start of 2026 to over US$100/ bbl since the war with Iran began, butas Bernstein's Energy team says, could potentially go much higher.⾃2026年初每桶60美元以来,油价在与伊朗开战后已飙升⾄每桶100美元以上,但正如伯恩斯坦的能源团队所⾔,油价可能会更⾼。How high oil price goes is dependent on the duration to which the Strait of Hormuz (SoH) is shut down.油价能涨到多⾼取决于霍尔⽊兹海峡(SoH)关闭的持续时间。Bernstein models three scenarios in attempt to answer the question:

伯恩斯坦设定三种情景以尝试回答该问题:

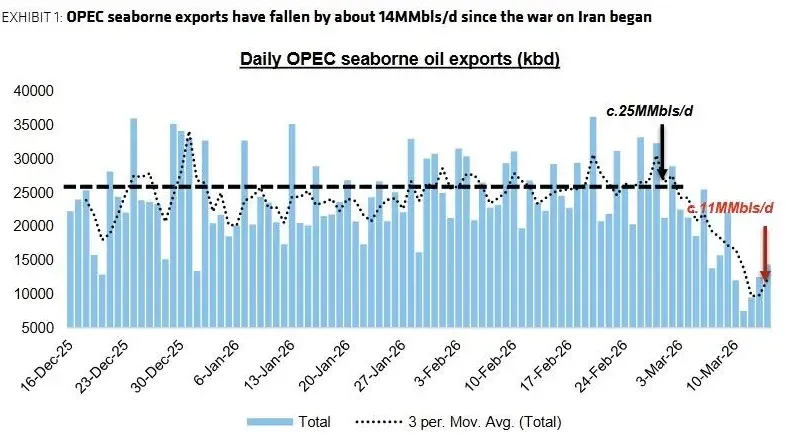

(b) three months and三个⽉停产情形(c) six months shut-down case.六个⽉停产情形。They see the potential for 15MMbs/d of supply disruption in a full SoH shut down case.他们认为在霍尔⽊兹海峡完全关闭的情形下,可能出现每⽇1500万桶的供应中断。According to tanker tracking data, OPEC crude and condensate loadings are down 13.8MMbls/d. In addition, there is a further 1.5MMbls/d of LPGdisruption from production in the Middle East.根据油轮追踪数据,OPEC原油和凝析油装载量减少了每⽇1380万桶。此外,中东地区产出的液化⽯油⽓还有每⽇150万桶的中断。This gives a total of 15.3MMbls/d of total liquid disruption in full Strait of Hormuz closure. For March where there were partial loading, the impact will be 10MMbls/d.这使得在霍尔⽊兹海峡完全关闭的情况下,总液体产量中断达到每⽇1530万桶。在三⽉份存在部分装载的情况下,影响将为每⽇1000万桶。While there could be some mitigations such as increased Red Sea lifting through East-West pipeline or Fujairah, it is equally possible that such routes are impacted by Iranian attacks.

虽然可以通过增加经东⻄管道或富查伊拉经由红海的出货来进⾏某些缓解,但同样有可能这些路线会受到伊朗攻击的影响。

Demand destruction could be in the range of 0.3-2.3MMs/d for 2026.

2026年的需求破坏可能在0.3–2.3MMs/d范围内。Higher oil price, disruption of air travel and shipping,and constraints on physical availability of oil products will could impact demand.

⾼的油价、航空旅⾏和航运中断以及⽯油产品实物可得性受限都可能影响需求。

In a one month shut down, the impact could be 1MMbls/d for two months giving annual disruption of 0.3MMMbls/d.

在为期⼀个⽉的停产中,影响可能为两个⽉内每天1MMbls,年化折算为每天0.3MMMbls。

in 3M and 6M close, we expect 2026 demand to contract by 1MMbls/d and 2.3MMbls/d respectively.

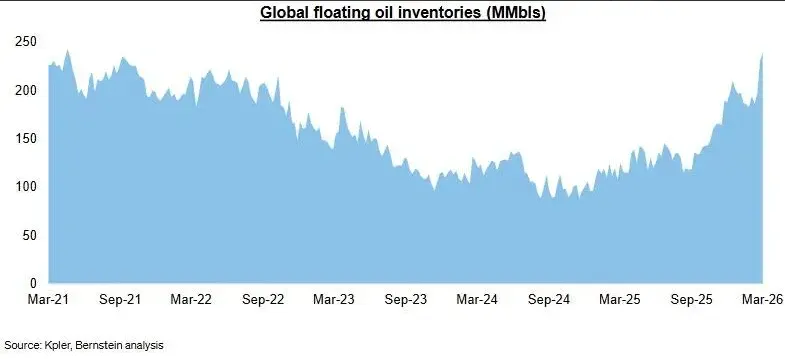

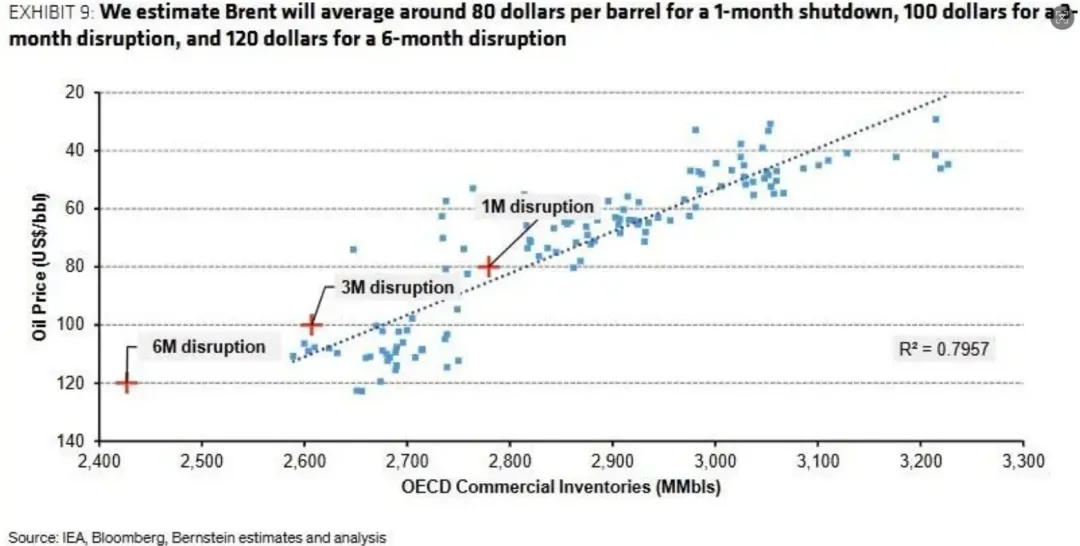

在3个⽉和6个⽉停产情况下,我们预计2026年需求将分别收缩每天1MMbls和2.3MMbls。Demand destruction in the 2008 global financial crisis was 2.4MMbls/d.2008年全球⾦融危机期间的需求破坏为240万桶/⽇。Liquidation of floating storage and SPR release could help cushion the loss of supply with a combined 550MMbls, but it is still not enough.浮动储油清算和战略⽯油储备(SPR)释放合计可提供5.5亿桶的缓冲,但仍不⾜以完全弥补供应损失。We assume 150MMbls of the 250MMbls of floating storage outside the Persian Gulf can be liquidated quickly.假设在波斯湾以外的2.5亿桶浮动储油中,有1.5亿桶可以迅速清算。此外,我们还假设4亿桶的SPR释放可在180天期间内卸出。Bernstein's analysis indicates a range of oil price from US$80-120/bbl for 2026 and a peak price of US$170/bbl in the 6M disruption case.Bernstein的分析显示,2026年油价区间为每桶80-120美元,在6个⽉中断情景下峰值为每桶170美元。If the SoH are reopened by the end of March,then US$100/bbl peak monthly and US$80/bbl annual price for Brent make sense. This remains our base case.

如果SoH在三⽉底前重新开放,则布伦特每⽉峰值100美元/桶、年均80美元/桶是合理的。这仍然是我们的基本情景。If on the other hand, disruption lasts 3M then we see an annual oil price of US$100/bbl and peak monthly price of US$140/bbl.另⼀⽅⾯,如果中断持续3个⽉,那么我们预计年均油价为每桶100美元,⽉度峰值为每桶140美元。In a 6M shut down, then US$120/bbl oil price for 2026 makes sense with a peak monthly price of US$170/bbl.在6个⽉停产的情况下,2026年油价为每桶120美元是合理的,⽉度峰值为每桶170美元。In the 3M to 6M shut down scenario, it seems inevitable that there would be a global recession in Bernstein's view.

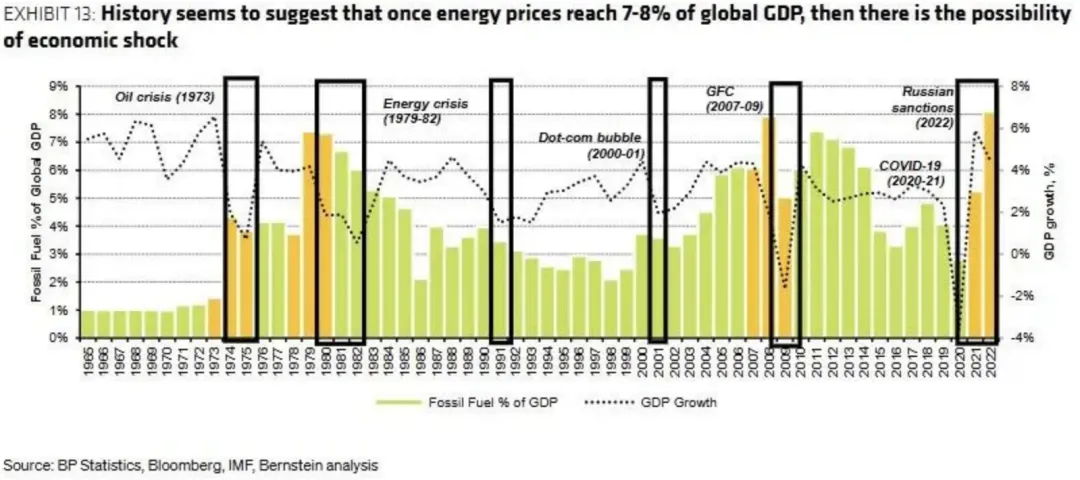

在Bernstein看来,在3个⽉到6个⽉的停摆情景下,全球经济陷⼊衰退似乎不可避免。Oil equities and markets more broadly are pricing in a short sharp conflict of one month.油⽓股和更⼴泛的市场正在反映出为期约⼀个⽉的短促剧烈冲突的预期。In our view, oil equities are pricing in US$80-100/bbl oil price this year, with a long term price of US$70/bbl.在我们看来,油⽓股今年正定价为80-100美元/桶的油价,⻓期油价为70美元/桶。This is consistent with a 1-3month shut down and no long term risk premium on oil price.这与1-3个⽉的停摆情景⼀致,并且对油价没有⻓期⻛险溢价。Similarly, markets more broadly are not pricing in a recession.Time will tell if this is correct, but given the economic consequences of a prolonged shutdown, we believe rationality will prevail and that a solution will be found in the coming days and weeks

时间将证明这是否正确,但鉴于⻓期停摆的经济后果,我们相信理性将占上⻛,并且在未来⼏天和⼏周内会找到解决⽅案。