最近在当前国际地缘政治复杂、国内两会召开的宏观背景下,我迫使自己学会去看各大投行的研报,以拓展自己的信息来源渠道。

原文-

China's National People's Congress set growth targets in line with expectations, but cyclical policies did not meet our expectations. Fiscal efforts for 2026 are largely unchanged, relying on the off-budget policy- financing tools. The tech push received much policy attention, while the new details on the widely watched consumption rebalancing are limited. Policy implementation would be the key thing to watch going forward, and the mid-year Politburo could be a window for recalibration in our view.

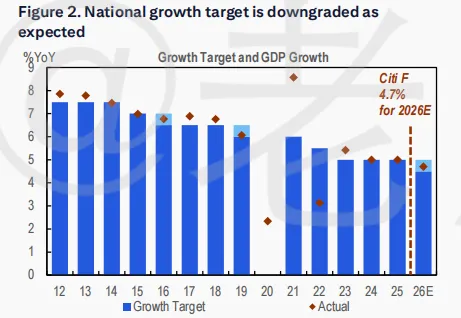

一、目标设定:意料之中的调降与“再通胀”的希望

Targets: the growth target is downgraded for the first time in four years as we had expected. Reflation receives explicit attention from the central government with the hope of reflation on the horizon now. Other structural targets, such as carbons emission, anti-involution, and the tech push were also well expected.

1、GDP目标下调

2、CPI目标维持

历年CPI目标

2025年:2%左右、2024年:3%左右、2023年:3%左右、2022年:3%左右、2021年:3%左右、2020年:3.5%左右

3、首次明确碳排放目标(-3.8%)

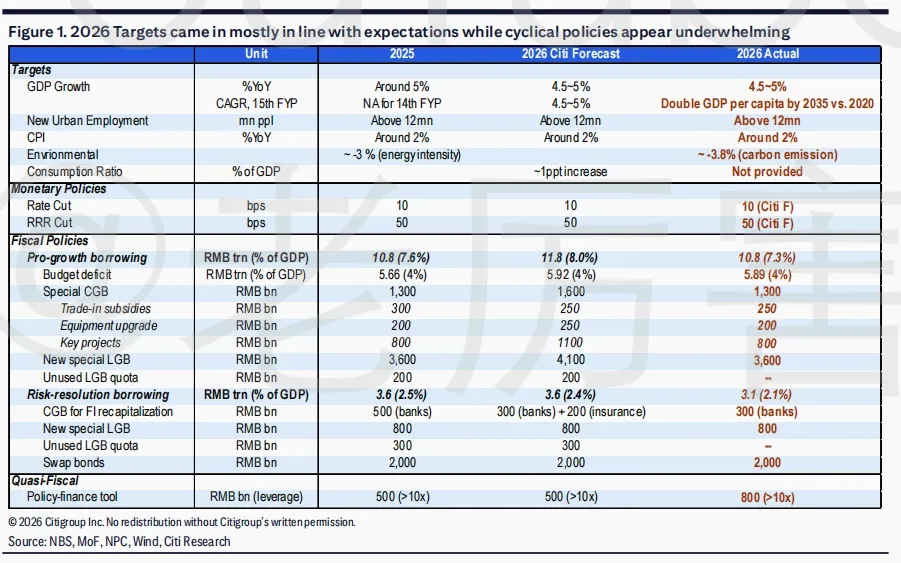

二、财政政策:有点“不够解渴”的周期性刺激

原文:

We hold our forecasts unchanged post today’s event. More details and clarity could come in the following days, especially regarding China’s 15th Five-Year Plan. Ongoing policy implementation would be essential to watch. The key variable for China macro this year is reflation in our view, which could still foster a nominal rebound in growth even as headline real growth inches down. The next window to recalibrate domestic policies could be the mid-year Politburo meeting.

原文:

SOE’s dividend payout could rise further according to the budget. It could be an effort to cushion revenue pressure, in our view. This could also have a direct impact on the equity market as well.

三、结构调整:科技是真金白银,消费还在等细则

1、先说科技端,那是真掏了真金白银的。

原文:

Today’s GWR offers a detailed and concrete action plan regarding the tech push.Emerging sectors such as AI and AI+ continue to receive strong policy attention,and this is not really a surprise following the detailed numeric targets in the provincial work reports. Regarding investment, the central government’s budgetary allocation for investment rises to RMB755bn from RMB735bn last year, a sign of the policy push for an investment rebound.

2、反观消费端,口号喊得很响,但细则还在天上飘。

原文:

Discussion on consumption rebalancing lacks the same granularity, although it ranks as the No.1 important task for this year. A numeric target for consumption ratio is not included for this year, and its inclusion for the 15th FYP remains to be determined. Related policy pledges are not new, with the details on implementation yet to be outlined.

3、常规操作

4、对外贸易的“端水艺术”。

原文:

The GWR mentions to expand imports for the first time since 2018-20. A further earlier mentioning of the same target was in 2013. It could be an olive branch, in our view, to China’s trading partners as China’s goods trade surplus inched close to US$1.2trn in 2025.

China’s agriculture and energy purchase could also receive greater attention in its engagement with the RoW, especially the US. Services opening could be steadily on going with the list expanding. 2025’s GWR mentioned telecom, healthcare, and education generally, while this year’s GWR highlights pilot programs in value-added telecom services, biotech, foreign-owned hospitals, as well as expansion of opening-up in the digital economy.

四、后续看点:紧盯落地执行与年中ZZ局会议

原文:

Policy implementation is the key thing to watch in the next few months. Local execution of property easing remains the most important thing to watch, in our view. PBoC’s monetary easing remains on the table, yet the timing could be complicated with a reflation outlook, deposits rollover and equity market rally. We expect the mid-year Politburo meeting to be a venue for policy recalibration if growth in the first half falls short of the target.

The geopolitical event calendar this year could be full with high-level exchanges between the US and China. We keep our expectations realistic, seeing no breakthrough but also no negative fallout for 2026. We maintain our view that the upcoming visit of President Trump to China may not yield substantial concrete results, but it could be sufficient to preserve the Busan consensus. The two countries could have mutual interests in China’s purchase of US goods, markets opening-up including bilateral investment, export control on chips and rare earth, RMB exchange rate and others.

1、先看内部:CPI的回升和A股的反弹

2、再看外部:特朗普访华与“不翻脸”底线

今年的地缘政治日历排得很满,最大的重头戏就是接下来特朗普的访华。对于中美互动,花旗的态度非常实在,总结起来就是八个字:没有突破,但没坏处。

免责声明:本文仅为个人学习记录与研报解读,不构成任何投资建议。市场有风险,投资需谨慎。所有观点基于公开信息,不代表任何机构立场。

本文研报:花旗银行 2026 年 3 月 5 日 《Citi China Economics:In-line Targets but Underwhelming Cyclical Policies – First Take from the NPC》

数据:国家统计局、政府工作报告公开数据